.avif)

.avif)

As an employer, if you are looking for a sustainable, realistic, and cost-effective way to enhance your benefit offerings and to attract and retain employees, a lifestyle spending account might just be what you need.

It’s easy to implement and administer and allows you to define its scope. At the same time, it gives your employees the freedom to spend funds on wellness-related services and products they choose.

Let's cover what a lifestyle spending account is, how it works, and why your business may need one.

Key Takeaways:

- A Lifestyle spending account is an effective employee engagement tool, allowing you to support diverse workforce needs.

- Employers customize the program to include eligible categories that best align with their organization’s core values — employees choose how to spend their money within the plan.

- Lifestyle spending accounts nicely supplement traditional benefits plans and help employers attract new employees and retain existing ones.

What is a Lifestyle Spending Account (LSA)?

Lifestyle spending accounts enable employers to offer flexible living benefits to their employees. Employers decide the scope of health and wellness expenses covered under these plans, allowing them to customize LSAs to align with company culture and values.

Also called a lifestyle account, specialty benefit, or perk allowance, an LSA typically includes a variety of spending categories, such as fitness, wellness, professional development, childcare, pet care, family activities, meals/food, commuting, and more.

According to SHRM, a company which aims to enhance the workplace and performance of employees within it, Lifestyle Spending Accounts (LSAs) are gaining traction among employers as a flexible benefit to meet diverse employee needs. According to a survey by WTW, 7% of employers currently offer LSAs, with an additional 38% planning or considering implementation by 2025.

This diversity gives employees the freedom to spend the funds on services that best fit their wants and needs. Your workforce is diverse, and your benefit program should reflect that. With an LSA, you can easily cater to your employees’ diverse needs.

Some features unique to LSAs include:

- Employers have full control over their LSAs. They get to decide all the aspects of the benefit program, including contribution limits, eligible expenses, allowance amount, and participation requirements.

- LSAs are typically taxable benefits for employees

- LSAs are easier to administer than traditional employee benefit programs

- LSAs provide a wider range of perks compared to FSAs (used for covering health-related costs) and HSAs (used for saving money on personal medical expenses)

How Does a Lifestyle Spending Account Work?

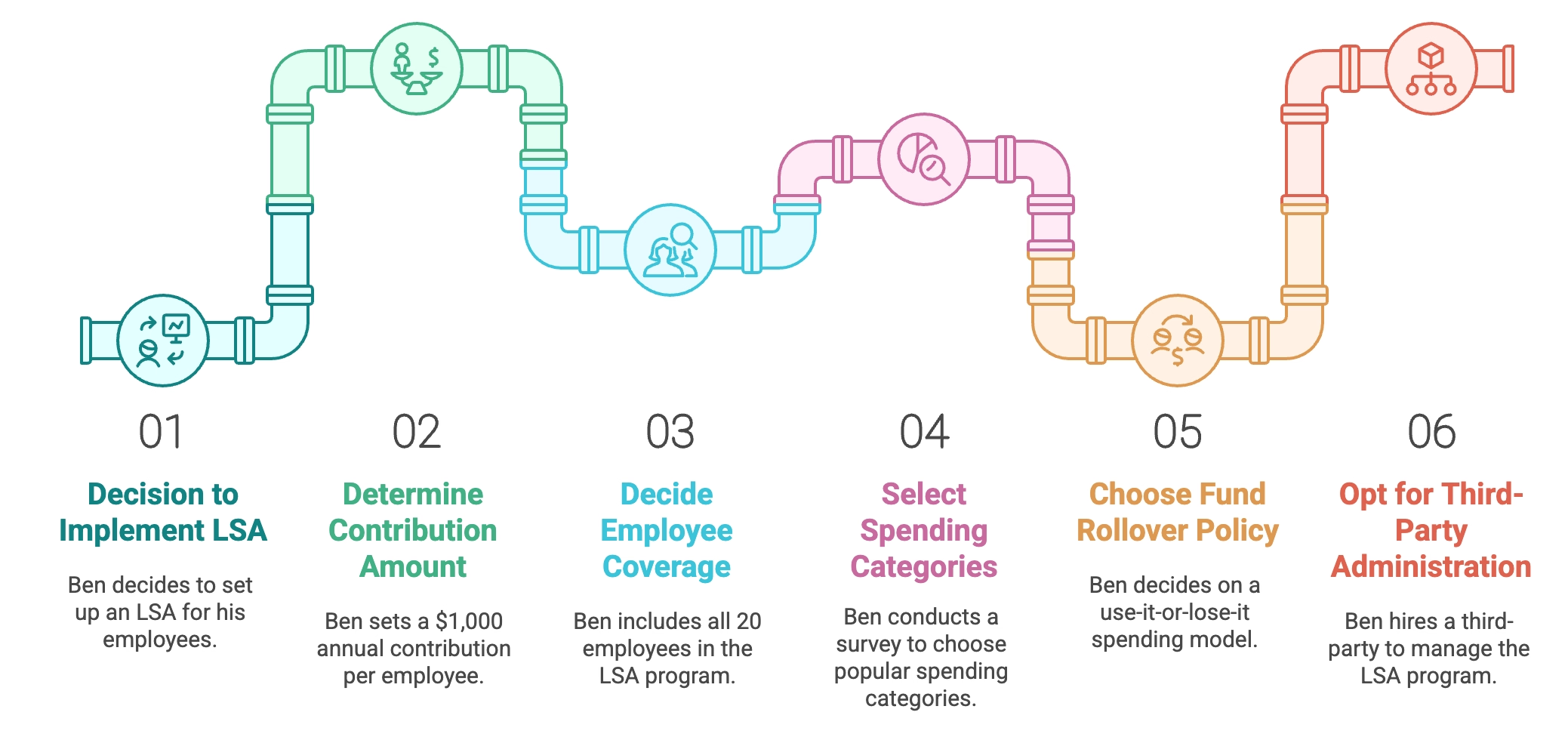

Here’s a real-life example that shows how an LSA works.

Ben owns a digital marketing agency and has 20 employees working for him. He knows he wants to set up a benefits program that helps improve the overall well-being of his employees. He chooses an LSA since it best matches his goals.

As an employer, Ben must first decide how much he would put into the LSA. He chooses to contribute $1,000 per employee per year.

Next, he needs to decide who will be covered, i.e., whether all employees or only a few (such as managers) will be covered. Because Ben wants to promote a healthy working culture, he extends the benefit program to each of his 20 employees.

Ben selects the eligible spending categories. Being a conscientious employer, he conducts an employee survey to find out which lifestyle benefits are most popular among his employees.

Once available expenses have been selected, Ben must decide if the LSA funds will roll over annually or run on a use-it-or-lose-it spending model. He also needs to determine how the benefit program will be administered.

While Ben could do this himself, he opted for a third party. This not only relieves Ben of the administrative work but also provides privacy to employees when submitting expenses. Now that everything is in order, Ben calls a staff meeting to explain the plan’s details to his employees.

Ben chooses a card-first approach for LSA benefits, which means his employees won’t have to go through the time-consuming process of submitting claims and waiting for reimbursement.

Since LSAs are taxable benefits, employees pay taxes on the money they spend. The value of these benefits is added to the employee's gross income, affecting their taxation based on local laws. Any unused funds are returned to Ben.

Setting Up a Lifestyle Spending Account

This is a straightforward process that requires careful consideration of several factors. Employers must decide which expenses will be covered by the LSA, set a reimbursement cap and other limits, determine how to manage the claiming process and inform employees about the program and its benefits.

When setting up a LSA, employers should assess the needs of their employees and research industry trends to determine which expenses to cover. This may include gym memberships, wellness programs, childcare services, and other lifestyle-related expenses. Employers should also consider what competing employers offer to stay competitive.

Employers must also set a reimbursement cap and other limits, such as time limitations or account balance expiration. This may include determining how much each eligible employee will get to spend and what kind of time limitations will be involved. Employers should also decide whether to offer a lump sum for the year or split it into monthly allowances.

If you’re unsure of where to begin, reach out to Dundas Life today. Through our expert life insurance advisors, we can provide you with the best plan to suit you and your employees needs.

Not an employer? No problem! Contact us today to find out what other kinds of life insurance you may be eligible for as an employee.

What eligible expenses can Lifestyle Spending Accounts be used for?

Most LSAs cover health and wellness expenses not covered by traditional benefit plans, but the sky is the limit. Here’s a list of typical expense categories and specific expenses that an LSA may cover:

Since options are practically limitless, an employer can customize the LSA to suit its employee’s wants and needs.

Benefits of a Lifestyle Spending Account

An LSA is a win-win for the employer and its employees, promoting employee wellness by encouraging participation in wellness programs and fostering a healthy work-life balance. It is easy and cost-effective to set up and administer and offers employees a ton of options, ensuring every one of them benefits from it.

Here are some of the main benefits of LSAs from both an employer’s and employee’s perspective.

Employer Benefits

- Helps attract top talent

Companies that offer a comprehensive, flexible benefits package attract the best talent.

A Glassdoor study states that benefits are an important factor for 60% of employees when considering a job offer. Another study claims almost 65% of millennials say they would rather earn less and enjoy their job than draw a higher salary and hate it.

So, if attracting the best talent is a priority, it makes sense to offer an LSA plan that will get prospective employees excited.

- Improve employee retention

A stellar fringe benefits package helps employees feel valued and appreciated, increasing job satisfaction and reducing turnover.

- Boosts productivity

There is a positive correlation between employee well-being and productivity. When your workers’ well-being is flourishing, your company directly benefits — they take fewer sick leaves, deliver better performance, and are less likely to experience burnout.

- Easier to administer and cost-effective

Compared to other employee benefits plans, LSAs are easier to administer. In addition, it allows employers to save money via the unused funds. For example, if a worker only spends $500 of the $1,000 allocated to her, you retain the unused $500.

Employee Benefits

- Flexibility

The key feature of an LSA is its flexibility, giving employees the freedom to make their own choices about how to improve their health and well-being. That might mean a water aerobic class one month and a Pilates class the next.

- Easy to use

Employees use a single account for different available expenses instead of navigating through multiple platforms to utilize their benefits.

- Help employees prioritize health & wellness activities.

While most people know they would enjoy a yoga retreat now and then or a monthly massage, they may not be comfortable spending money on them when they could use it to buy more “practical” things. However, with an LSA in place, they have access to funds created specifically for their physical and emotional well-being. This encourages them to spend money on services and products important to their wellness without feeling guilty about it.

Plan Administration and Management

Plan administration and management are critical components of a successful Lifestyle Spending Account program. Employers should set up a clear claims process, including whether receipts are required, and communicate the guidelines to employees.

They should also review spending reports regularly to track usage and adjust offerings as needed. This may involve auditing the program periodically to identify problems and signs of fraud. By regularly reviewing the program, employers can ensure that it is meeting its intended goals and making adjustments as needed.

Notable insurance companies that provide LSA’s include Garriet Agencies. Sun Life offers a Personal Spending Account (PSA) which functions similarly to an LSA. Canada Life and Manulife also offer Health Care Spending Accounts (HCSA), used to cover medical expenses.

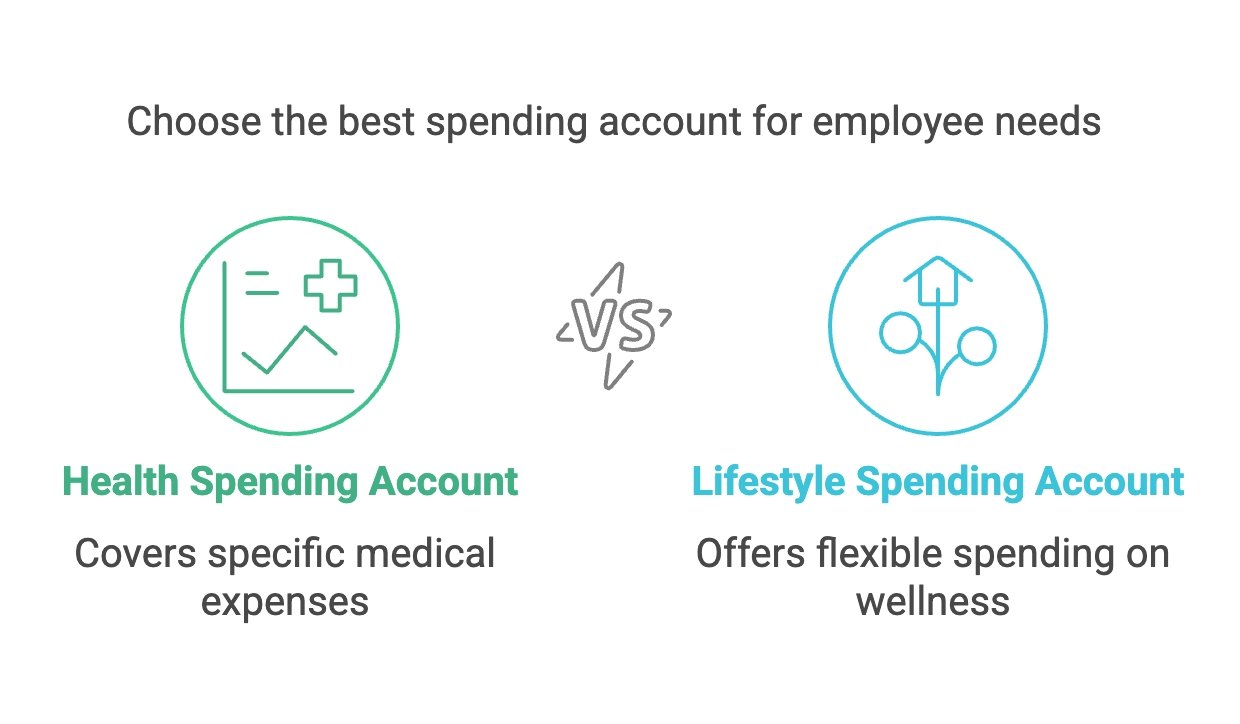

Difference between a Health Spending Account and a Lifestyle Spending Account

A health spending account helps employees pay for medical expenses recognized under Canada’s Income Tax Act, such as prescription drugs, dental fees, eyeglasses, physiotherapy, and more. Lifestyle spending accounts, in contrast, allow employees to spend money on a broad range of personal, everyday wellness needs determined by the employer, offering more flexibility compared to traditional accounts like a health savings account or a flexible spending account.

Measuring Success and ROI

Measuring the success and return on investment (ROI) of a Lifestyle Spending Account program is essential to determining its effectiveness. Employers can measure success by tracking employee participation rates, employee satisfaction, and retention rates. Employers can also measure the ROI by tracking the cost savings associated with reduced turnover and improved productivity.

Employers can use various metrics to measure the success of their LSA program, including:

- Employee participation rates: Track the number of employees who participate in the program and the types of expenses they submit for reimbursement.

- Employee satisfaction: Conduct surveys or focus groups to gauge employee satisfaction with the program and identify areas for improvement.

- Retention rates: Track employee retention rates to determine if the program is having a positive impact on employee turnover.

- Cost savings: Track the cost savings associated with reduced turnover and improved productivity.

Employee Retention and Satisfaction

Lifestyle Spending Accounts can have a significant impact on employee retention and satisfaction. By offering a flexible and customizable benefits package, employers can demonstrate their commitment to their employees’ overall well-being and quality of life.

Research has shown that employees who are satisfied with their package are more likely to be engaged and productive at work. A survey by Glassdoor found that 94% of employees want benefits that positively impact their overall well-being. By offering a Lifestyle Spending Account, employers can provide employees with a valuable benefit that can help them achieve their health and wellness goals.

According to forma, an employee benefits company, COCC was able to increase performance by launching an inclusive LSA program. COCC, a leading technology solution provider for banks and credit unions, recognized the evolving needs of its 800 employees and sought to offer more equitable benefits. In January 2023, they launched an LSA program to provide flexibility and inclusivity in their benefits offerings. This initiative led to a significant increase in employee engagement and satisfaction, demonstrating the effectiveness of LSAs in addressing diverse workforce needs.

Implementation and Launch

Implementing and launching a Lifestyle Spending Account program requires careful planning and execution.

- Employers should start by communicating the program to employees and providing them with information about the program and its lifestyle benefits.

- Employers should also establish a system for managing the claiming process and ensure that employees understand the process. This may involve providing employees with a user-friendly online portal or mobile app to submit expenses and track their account balances.

- Employers should also consider partnering with a benefits administration provider to help manage the program and ensure compliance with relevant laws and regulations. By partnering with Dundas Life, employers can ensure that their program is administered efficiently and effectively.

- Clearly defining what expenses qualify—such as fitness memberships, wellness programs, or professional development— and spending guidelines helps employees make informed decisions about how to use their funds. Providing a comprehensive FAQ document or host a Q&A session to address common concerns and improve participation rates.

- Once the program is live, employers should regularly review employee usage patterns and feedback to determine whether adjustments are needed. If certain benefits are underutilized, expanding the range of eligible expenses or increasing awareness through internal communications can enhance engagement. Periodic employee surveys can provide valuable insights into how the LSA contributes to overall job satisfaction and well-being.

Conclusion

A lifestyle spending account is an employee-sponsored, fully customizable benefit. The employer chooses the activities on which the funds can be spent, as well as the dollar amounts, funding frequency, and reimbursement processes. Then, the individual employees can spend the money in their LSA accounts as they wish. Compared to traditional flexible spending accounts and health savings accounts, LSAs offer broader health wellness expense coverage tailored to individual needs.

Looking to setup an Lifestyle Spending Account or other employee benefits plan? Book your call with a Dundas Life licensed advisor today.

Frequently Asked Questions (FAQs)

Can Lifestyle Spending Accounts be used to cover expenses for my dependents?

Yes, lifestyle spending accounts may cover allowed expenses for an employee’s dependents, like a spouse or children. However, coverage details vary from one lifestyle spending account to another. Read your plan’s terms to find out if it covers your dependents.

What happens to the funds in my Lifestyle Spending Account if I leave my job or change employers?

Typically, your LSA is directly linked to your employment status. You will likely lose access to it if you leave your job or switch employers.

How do Lifestyle Spending Accounts impact my taxes?

A Lifestyle Spending Account is a taxable benefit. This means the amount you spend will be taxed. For example, if you receive $1,500 a year in your LSA and spend $1,000, you’ll pay income tax on that amount (and not the full amount).

Can Lifestyle Spending Accounts be used for professional development or continuing education expenses?

Most LSAs include multiple spending categories, including professional development or continuing education expenses. However, since each LSA plan is unique and the employer decides the eligible categories, read the plan’s document to determine whether coverage extends to these expenses.

How often can I submit reimbursement requests for Lifestyle Spending Account expenses?

How frequently you can submit claim requests depends on your plan’s details. Generally, employees can submit claim requests on a regular basis, such as monthly, quarterly, or bi-yearly. Some plans follow a card-first approach, allowing employees to pay for allowed expenses using a special payment card. Read your plan’s document to determine whether you first need to pay out-of-pocket and, if yes, what the reimbursement procedure is.

%20(1)%20(1).png)

-p-500.png)

.avif)